特殊目的收購公司(SPAC) 是一種空殼公司,上市籌集資金的目的是爲了上市後一段預設期限內收購目標公司(SPAC併購目標)的業務(SPAC併購交易)。

SPAC上市機制於 2022 年 1 月 1 日生效

- 有至少一名SPAC發起人為證監會持牌機構並持有至少10%發起人股份。

- SPAC投資者僅限於專業投資者。

- SPAC必須從其首次發售至少籌集10億港元的資金。

- 完成SPAC併購交易後的上市公司須符合所有新上市規定。

- SPAC必須向獨立第三方投資者籌集至少SPAC併購目標議定估值的5%至25%的投資額以完成SPAC併購交易。此獨立第三方投資者必須為專業投資者。獨立第三方投資至少要有50%來自至少三名資深投資者。

SPAC上市機制主要特徵

SPAC併購交易前

- 於SPAC併購交易之前,SPAC證券將僅限專業投資者認購和買賣。

- SPAC證券須分發予至少75名專業投資者,當中須有至少20名機構專業投資者,而此等機構專 業投資者必須持有至少75%的待上市SPAC證券。

- SPAC發起人須符合嚴格的適合性及資格規定,且必須有至少一名爲第6類或第9類證監會持牌公司並持有至少10%發起人股份。聯交所會考慮按個別情況授予豁免(例如:接受持有相等於 證監會第6類及/或第9類牌照的海外認證的SPAC發起人)。

- SPAC的董事會須至少有兩人是第6類或第9類證監會持牌人(包括一名代表持牌SPAC發起人的董事)。

- 發起人股份限於SPAC上市時已發行股份總數的30%。

- SPAC權證及發行人權證限於有關權證發行時已發行股份數目的50%。

- SPAC必須從其首次發售至少籌集10億港元的資金。

- SPAC股份的證券簡稱會以標記「Z」結尾。

SPAC併購交易

- 完成SPAC併購交易後的上市公司(繼承公司)須符合所有新上市規定(包括委聘首次公開發售保薦人進行盡職審查、最低市值規定及財務資格測試)。

- SPAC併購目標公平市值須達自SPAC首次發售所籌得資金的至少80% 。

- SPAC必須獲得獨立第三方投資(獨立PIPE 投資)以完成SPAC併購交易,而該有關投資須佔SPAC併購目標議定估值的至少5%至25% 。PIPE 投資者均須為專業投資者。

- 有至少50%的獨立PIPE 投資須來自至少三名資深投資者。

- SPAC併購交易須經SPAC股東於股東大會上批准作實( 但不包括SPAC 發起人及其他擁有重大權益的股東)。

- SPAC股東在以下事宜發生前須有權贖回其股份: (a)SPAC併購交易;(b)SPAC發起人以及/ 或SPAC 董事有重大變動;及(c)延遲任何物色適合的SPAC 併購目標的期限。

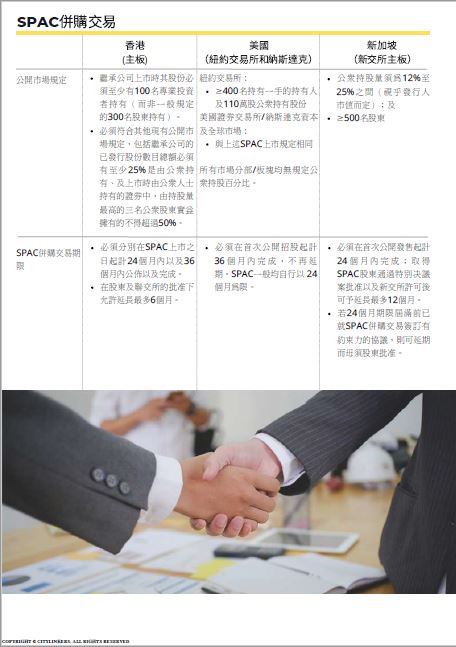

- 繼承公司上市時其股份必須至少有100名專業投資者持有(而非一般規定的 300名股東持有)。

- SPAC併購交易必須分別在SPAC上市之日起計24個月內公布以及36個月內完成,而此期限可 在SPAC股東及聯交所的批准下延長最多六個月。